What is FIFO and why does my employer ask for LAFHA declaration?

In Australia, many workers in industries such as mining, oil and gas, construction, and large infrastructure projects operate under FIFO (fly-in fly-out) arrangements. Under this setup, employees travel to remote job sites for rostered periods and stay there temporarily, while maintaining their usual home in another location—often in a major city. Because FIFO workers are […]

Should I buy an investment property in a trust in Australia?

Buying an investment property through a trust is a strategy commonly used by property investors in Australia who want flexibility in income distribution, asset protection, and long-term tax planning. However, whether a trust structure is appropriate depends on your personal financial situation, your tax position, and your long-term investment strategy. A trust is a legal […]

What is FIFO and why does my employer ask for LAFHA declaration?

Should I buy an investment property in a trust in Australia?

Can a Director Invoice Their Own Company or Trust and Receive Director Fees Through Another Entity?

Can I avoid a division 7A deemed dividend by repaying a company loan before 30 June and withdrawing the money again after 1 July?

Can I claim tax deductions on a holiday home in Australia?

How much can I claim for my home electricity when charging my electric vehicle?

What Is the 45-Day Rule for Franking Credits?

How can I ensure that only my children and family benefit from my assets and property portfolio?

If you own a holiday home in Australia, you cannot automatically claim full tax deductions. Under current Australian Taxation Office guidance, holiday home tax deductions may be denied if the property is not mainly held to earn rental income, even if it is rented out for part of the year.

The ATO’s view is that where a holiday home is used significantly for private or personal purposes, the leisure facility rules in section 26-50 can prevent deductions such as loan interest, council rates, land tax, and repairs and maintenance. In simple terms, if the property looks more like a lifestyle asset than a genuine rental property, the deductions are at risk.

The ATO has acknowledged that this position was not clearly communicated in earlier guidance. As a result, it has confirmed it will not actively review holiday home deductions incurred before 1 July 2026, provided the arrangement was entered into before 12 November 2025. This transitional relief gives existing holiday homeowners time to review how their property is used and structured.

Where a holiday home is used partly to earn rental income and partly for private use, expenses must be apportioned on a fair and reasonable basis. Accepted methods include time-based apportionment, area-based apportionment, or a combination of both. Any alternative method must be clearly supported if reviewed.

The ATO applies a risk-based approach. Holiday homes that are genuinely available for rent at market rates, especially during peak periods, and used minimally for personal purposes are considered lower risk. Properties where personal use is prioritised, peak periods are blocked out, or rental efforts are limited are considered higher risk and more likely to attract attention from the Australian Taxation Office.

The key takeaway is that holiday home tax deductions depend on commercial intent, not ownership alone.

It is important to note that the land tax amount is not deductible in the year you pay it. Instead, deductions must be taken in the respective income years to which the land tax liabilities related to. It’s crucial to understand that your liability for land tax is determined by the usage of the property within a given year, regardless of when the tax assessment is actually issued.

When you pay land tax for past years (known as paying “in arrears”), you can’t deduct this payment from your income for the year in which you make the payment. Instead, you can only claim a deduction for the land tax in the years that the tax was originally due for.

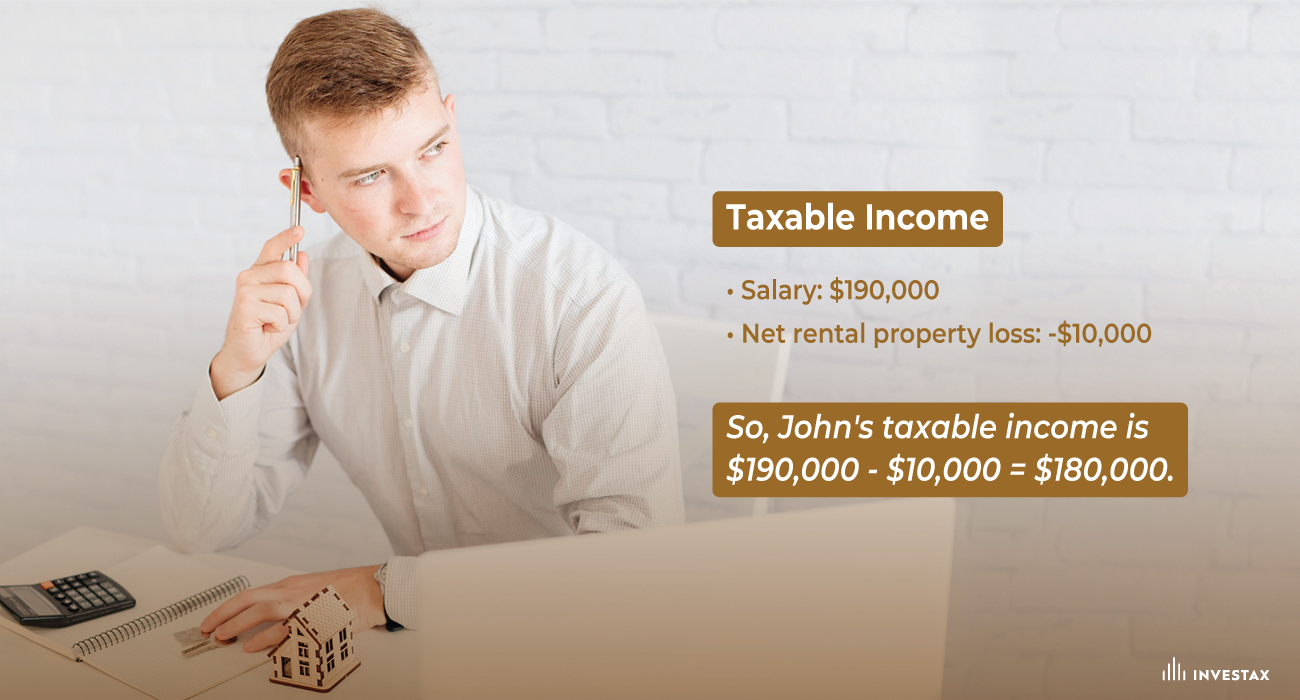

For an example – Imagine it’s 2024, and John receives a bill for land tax for the years 2022 and 2023 that he hasn’t paid yet. Even though John pays this bill in 2024, he can’t claim the deduction on his 2024 tax return. Instead, he should claim the deduction for the 2022 land tax on his 2022 tax return, and the deduction for the 2023 land tax on his 2023 tax return, because those are the years the tax relates to, even though he paid it later.

You can claim land tax as a tax deduction for your investment properties. However, you cannot claim land tax as an immediate deduction if your property is not generating rental income or if you are using the property for personal use.

You are eligible to deduct expenses including interest on loans, local council, water and sewerage rates, land taxes, and emergency services levies incurred during the period of renovating a property intended for rental. It’s important to note, however, that your eligibility for these deductions ceases once your intentions for the property change, such as deciding to use it for personal purposes instead.

According to GSTR 2012/6 Airbnb doesn’t fall under commercial residential premises. The definition of ‘commercial residential premises’ in section 195-1 includes the following seven paragraphs, none of which indicate anything similar to Airbnb. This distinction is crucial for understanding the regulatory and tax implications associated with offering or operating Airbnb properties.

- a hotel, motel, inn, hostel or boarding house.

- premises used to provide accommodation in connection with a school;

- a ship that is mainly let out on hire in the ordinary course of a business of letting ships out on hire.

- a ship that is mainly used for entertainment or transport in the ordinary course of a business of providing ships for entertainment or transport.

- a marina at which one or more of the berths are occupied, or are to be occupied, by ships used as residences.

- a caravan park or a camping ground; or

- anything similar to residential premises described in paragraphs (a) to (e).

Check out our Comprehensive Guide To Converting Your Long-Term Investment Property To Airbnb Or Short-Term Rental for further information.

Reference – https://www8.austlii.edu.au/au/other/rulings/ato/ATOGSTR/2012/GSTR20126.pdf

The goods and services tax (GST) does not apply to residential rents, so Airbnb hosts do not have to pay it. This also means that you can’t get a GST credit for the costs that go along with it. This is applied even if your sales are more than $75,000, which is the GST threshold.

Please check feel free to check out our Tax Consequence guide for Airbnb.

Many investors begin their investment journey without considering estate planning or asset protection. It is only after they build a substantial asset base or experience major life events such as divorce, a family death, or financial difficulties that they start thinking about how to protect their assets and pass them on to their children. If you hold assets in your personal name and want to ensure that your children and grandchildren are the ones who benefit from those assets, a testamentary trust is one of the most effective ways to keep your property portfolio within the family after your passing.

Established through your Will, it allows your assets to be managed by trusted individuals (trustees) for the benefit of your chosen beneficiaries — typically your children and family members.

Unlike direct inheritance, which transfers ownership immediately, a testamentary trust gives you greater control and protection. It helps safeguard family wealth from potential risks such as divorce settlements, bankruptcy, or financial mismanagement by beneficiaries. You can also specify how and when your children access their inheritance, ensuring financial discipline and long-term benefit.

From a tax perspective, testamentary trusts offer valuable flexibility. Income distributed to minor children can be taxed at ordinary adult rates, not at the penalty rates usually applied to minors, which can lead to significant family tax savings.

If your goal is to ensure your wealth supports only your intended family members while providing both protection and flexibility, a testamentary trust can be a crucial component of your estate planning.

A testamentary trust is one of the most effective ways to ensure your assets and property portfolio remain within your family after your passing. Established through your Will, it allows your assets to be managed by trusted individuals (trustees) for the benefit of your chosen beneficiaries — typically your children and family members.

Unlike direct inheritance, which transfers ownership immediately, a testamentary trust gives you greater control and protection. It helps safeguard family wealth from potential risks such as divorce settlements, bankruptcy, or financial mismanagement by beneficiaries. You can also specify how and when your children access their inheritance, ensuring financial discipline and long-term benefit.

From a tax perspective, testamentary trusts offer flexibility. Income distributed to minor children can be taxed at ordinary adult rates, not at the penalty rates usually applied to minors, which can lead to significant family tax savings.

If you want your wealth to support only your intended family members and provide both protection and flexibility, a testamentary trust can be an essential part of your estate planning.

Yes, you can purchase a car in the name of your trust. However, whether you can claim a tax deduction for it is not a straightforward answer. It depends on how the car is used and the nature of your trust’s activities.

What Does Your Trust Do?

🔹 Investment Trust (Property or Shares):

If your trust is primarily used for passive income activities, such as holding rental properties or shares, then there is no clear business connection to justify claiming tax deductions for the vehicle. In this case, the car is likely to be used for personal purposes, which means deductions are generally not allowed.

🔹 Active Business Trust:

If the trust actively operates a business—such as a consulting firm, construction company, or retail store—then there may be a valid business reason for purchasing the vehicle. In this case, tax deductions may be available, provided the car is genuinely used for business purposes.

Fringe Benefits Tax (FBT) Considerations

Owning a personal-use vehicle in a trust can sometimes create additional tax reporting requirements because Fringe Benefits Tax (FBT) may apply.

If the trust provides a car to a trustee, employee, or beneficiary for personal use, the trust may be liable for FBT. This tax applies when a vehicle is used for non-business purposes, and it can significantly impact the overall tax benefit.

Starting your investment journey, whether as an employee or a business owner, requires careful consideration of two critical aspects: tax planning and asset protection. These are not just checkboxes on a list; they are foundational pillars that seasoned investors prioritise from the outset. The goal is not merely to accumulate assets but to do so in a way that ensures their longevity and protection.

Asset protection is all about creating a secure environment for your investments. It’s the practice of arranging your assets in a way that minimizes the risk of loss, whether through legal challenges, business debts, or other financial liabilities. The essence of asset protection lies in the foresight to anticipate potential risks and to structure your investments in a way that those risks are mitigated before they can even arise.

Transferring existing property and assets to a trust or company for asset protection purposes is possible, but it must be done carefully and in compliance with the law. Such transfers can have tax consequences, including capital gains tax (CGT) and stamp duty. CGT may apply if the transfer results in a capital gain, and stamp duty may be levied depending on your jurisdiction. Additionally, anti-avoidance provisions are in place to prevent tax evasion through asset transfers. It’s crucial to seek legal and tax advice before proceeding to understand the implications and ensure compliance with tax laws and regulations. Each case is unique, and a tailored approach is essential to address both asset protection and tax considerations.

The 5-year clawback period, often associated with bankruptcy law, refers to a period of time preceding a debtor’s bankruptcy filing, typically starting from the date of the bankruptcy filing. During this period, a bankruptcy trustee has the authority to review, and potentially reverse certain transactions made by the debtor, such as preferential payments to specific creditors or fraudulent asset transfers. The purpose is to prevent debtors from attempting to shield assets from creditors by engaging in questionable financial transactions shortly before declaring bankruptcy.

While it is possible to transfer properties and assets to a trust or a company, doing so with the intent to evade legitimate creditors or legal claims can have serious legal consequences. Transfers made with the intent to hinder, delay, or defraud creditors are typically considered fraudulent and can be challenged by creditors or the court. Australia, like many jurisdictions, has laws in place to prevent fraudulent asset transfers. It’s essential to consult with legal professionals to ensure any asset protection or restructuring measures are done within the bounds of the law and do not violate legal obligations to creditors or the court.

No, asset protection strategies cannot provide absolute protection from all types of legal claims or creditors. Certain legal claims, such as child support, alimony, or government obligations, may not be shielded by asset protection measures. Additionally, fraudulent or improper transfers intended to evade legitimate creditors can be challenged and deemed ineffective. Asset protection is best used as a proactive strategy to minimize risks rather than as a guarantee against all possible legal challenges. Consultation with legal and financial experts is crucial for tailored asset protection planning.

Asset protection is entirely legal when done within the boundaries of the law and regulatory requirements. It involves prudent financial planning and the use of legal mechanisms to protect assets from unforeseen risks. Engaging in fraudulent activities or hiding assets to evade legitimate creditors is illegal and can result in severe legal consequences.

Asset protection refers to strategies and legal mechanisms investors and businesses use to safeguard their assets from potential creditors, lawsuits, or financial risks. It’s crucial because it helps protect your hard-earned assets from being seized or depleted in the event of legal disputes, bankruptcy, or unforeseen financial challenges, ensuring the preservation of your wealth.

From 1 July 2025, interest charged by the ATO on outstanding tax debts will no longer be tax deductible. This includes both the General Interest Charge (GIC) and Shortfall Interest Charge (SIC) that the Australian Taxation Office applies when tax is paid late or underpaid.

Until 30 June 2025, you can still claim these ATO interest charges as part of your cost of managing tax affairs. But from the 2025–26 financial year onwards, that deduction will be removed. This means any ATO interest incurred after 1 July 2025 will become a non-deductible expense, increasing the after-tax cost of carrying ATO debt.

For business owners, one potential strategy is to refinance the ATO debt using a business or equity loan. The interest on a genuine business loan remains tax deductible if the borrowed funds are used for an income-producing purpose, such as paying down ATO liabilities. In addition, commercial loan interest rates are usually much lower than ATO interest rates, which makes refinancing both tax-effective and cost-efficient.

If you’re unsure how this change affects your business or whether refinancing makes sense in your case, speak with the tax specialists at Investax Group. Our accountants can help you assess your options and implement the most effective tax strategy for your outstanding ATO tax debts.

Scammers are getting smarter every day when it comes to targeting Australians. They’ll try all sorts of tricks to get your personal or business details—like phone calls about fake tax debts or emails promising a surprise tax refund. To keep both you and your business safe this tax season, especially with email and SMS scams on the rise, the Australian Taxation Office suggests three simple but important precautions:

- Avoid clicking on unsolicited links or scanning QR codes in emails or texts claiming to be from the ATO. These messages may be phishing attempts designed to steal your sensitive corporate credentials.

- Always access ATO services by manually typing the URL into your browser, rather than clicking through links. This ensures you’re visiting the legitimate ATO site and not a spoofed imitation.

- Never share your Tax File Number (TFN), Australian Business Number (ABN), or login details (like myID or RAM) unless you’re absolutely sure the request is genuine and the recipient is verified. Keeping these details confidential helps protect against identity fraud.

Extra Safety Tip: If you get a suspicious call, SMS, voicemail, email, or even a social media message claiming to be from the ATO, don’t respond or engage. Remember, if you have a registered tax agent or accountant, the ATO will usually contact them first—not you directly. If someone calls saying they’re from the ATO, don’t get drawn into the conversation. Instead, hang up and call the ATO yourself on their official number to check if the contact was genuine.

Top 3 Scam Awareness Tips – ATO

If you have purchased a property within your Self-Managed Super Fund (SMSF) using a Limited Recourse Borrowing Arrangement (LRBA), you might be wondering whether you can carry out major renovations to enhance the property. The rules around this are strict and set out by the Australian Taxation Office (ATO) in SMSFR 2012/1 and getting them wrong can put your SMSF in breach of superannuation law.

What You Can Do with Borrowings

Under LRBA, borrowed funds can only be used for:

- Repairs – fixing damage or defects to restore the property to its original state (e.g., replacing a roof damaged by a storm, repairing fire damage to a kitchen).

- Maintenance – work that prevents deterioration and keeps the property functional (e.g., painting walls, replacing worn fences, renewing an outdated kitchen with modern equivalents).

These works are allowed because they don’t fundamentally change the character of the property.

What You Cannot Do with Borrowings

Major renovations that significantly improve or alter the property cannot be funded with LRBA borrowings. Examples include:

- Adding a second storey, new rooms, or additional bathrooms.

- Constructing a granny flat, swimming pool, or pergola.

- Converting a residential property into a commercial property or multiple strata-titled units.

Such works are classified as improvements, and LRBA rules prohibit borrowed funds from being used for improvements. Doing so could cause your SMSF to breach section 67A of the SIS Act.

How Major Renovations Can Be Done

While you can’t use borrowings for major renovations, you may proceed if:

- You fund the renovations using SMSF’s own cash resources (contributions or accumulated earnings).

- The renovations don’t transform the property into a different asset type (e.g., it must remain residential if originally purchased as residential).

- It doesn’t result in a different asset being held (for example, converting a house into a block of units would breach LRBA rules).

A Bare Trust is essential when a Self-Managed Super Fund (SMSF) borrows money to buy a property, creating a structure that separates the property from other assets in the SMSF. This setup, known as a Limited Recourse Borrowing Arrangement (LRBA), ensures that the lender’s recourse is limited only to the property purchased with the borrowed funds, safeguarding the remaining SMSF assets. By law, a Bare Trust is required to facilitate this protective arrangement, as it legally holds the property on behalf of the SMSF.

Beyond regulatory compliance, a Bare Trust adds a critical layer of asset protection. Should any issues or claims arise related to the loan or property, only the property within the Bare Trust is at risk, protecting the other assets within the SMSF from potential legal or financial complications. This structure not only adheres to SMSF borrowing laws but also aligns with the long-term goals of SMSF investors seeking both growth and security in their property investments.

A bare trust in a Self-Managed Super Fund (SMSF) is a popular structure used to hold an asset, typically a property, when a SMSF implements a Limited Recourse Borrowing Arrangement (LRBA) strategy. A bare trust is a fundamental form of trust arrangement where a trustee is designated to hold property or assets solely on behalf of a clearly identified beneficiary. In this instance, the Self-Managed Super Fund (SMSF) is the ultimate beneficiary. In this type of trust arrangement, the trustee’s role is notably minimal and straightforward, primarily involving the safeguarding and eventual transfer of the trust property to the beneficiary once the loan is paid off, upon the beneficiary’s request.

The trustee, in this context, does not possess discretionary powers or extensive duties beyond this basic obligation. The essence of a bare trust lies in the absolute entitlement of the beneficiary’s’ to both the capital and the income generated by the trust’s assets. For CGT purposes, any disposal of the assets of the trust by a bare trustee will be treated as a disposal by the beneficiary i.e. the SMSF.

Source – ATO – Absolute entitlement

Yes, it is highly recommended to seek legal advice when setting up a Bare Trust for SMSF property investment. Legal professionals can ensure the trust structure complies with all relevant regulations and help draft the necessary legal documents.

When selling the property, the proceeds will typically go back to the SMSF, as it holds the beneficial ownership. According to the SMSF’s investment strategy, the funds can then be reinvested or used for retirement benefits.

Yes, there are rules and restrictions to be aware of:

• The property held in the Bare Trust must meet the sole purpose test of providing retirement benefits to SMSF members.

• The Bare Trust cannot hold more than one property

• The Bare Trust must not be used for any purpose other than holding the property for the SMSF.

• The SMSF is the only entity that can benefit from the property held in the Bare Trust.

While the Bare Trustee holds the legal title, the SMSF has control over property management and decision-making. The SMSF trustee has the authority to make decisions about the property, including leasing, selling, and maintaining it, in line with superannuation laws.

Yes, you can use a Bare Trust for both residential and commercial property investments. However, the same rules and restrictions apply, including compliance with the sole purpose test and other SMSF regulations.

A Bare Trust is commonly used in SMSF property investment to comply with superannuation and legal regulations. It separates the legal ownership (held by the Bare Trustee) from the beneficial ownership (held by the SMSF), ensuring that the property investment aligns with SMSF rules.

A Bare Trust, often used in Self-Managed Super Fund (SMSF) property investments, is a legal arrangement where a trustee holds property or assets on behalf of the SMSF. It is a transparent trust structure where the SMSF holds the beneficial ownership of the property, while the Bare Trustee holds the legal title.

Choosing a company or trust structure for your business over a sole trader or partnership offers several advantages. These structures provide limited liability, protecting your personal assets from business debts, making them appealing for risk management. Trusts, particularly discretionary trusts, offer tax efficiency through income distribution among beneficiaries. They also serve well for asset protection and estate planning, allowing for the orderly transfer of assets. Companies, with separate tax rates and perpetual existence, are attractive to investors and convey professionalism, while also facilitating business continuity and scalability. Depending on your specific business goals, legal requirements, and financial situation, consulting with experts such as accountants or legal advisors can help determine the most suitable structure for your needs.

Yes, it is possible to have multiple business structures for different aspects of your business, such as a company for one division and a trust for another. Each structure will have its own legal and tax implications.

Tax implications vary by structure. Sole traders report business income on their individual tax return. Companies pay tax on their profits at the corporate tax rate. Partnerships and trusts distribute profits to partners or beneficiaries who report them on their individual tax returns.

The most common business structure in Australia is the sole trader structure, followed by companies, Trust and partnerships. The choice of structure depends on factors like liability, taxation, and business goals.

Choosing the right structure depends on factors like the nature of your business, liability preferences, tax implications, and future growth plans. Consult with a business advisor or accountant for personalized advice.

If you are a New Zealand citizen living in Australia on a Subclass 444 Special Category Visa, you are generally classed as a “temporary resident” for tax purposes — even though you may also be considered an Australian resident for tax purposes.

Under the ATO’s temporary resident rules, you only pay tax in Australia on your Australian-sourced income, such as:

- Salary or wages earned in Australia

- Rental income from Australian property

- Dividends from Australian shares

You do not pay tax on most foreign-sourced income or capital gains (for example, from overseas property or foreign shares), provided you:

- Hold a Subclass 444 visa, and

- Do not have an Australian citizen or permanent resident spouse/de-facto partner.

When could you lose your temporary resident status for tax purposes?

The ATO may revoke your temporary resident classification if you are in a spousal or de-facto relationship with an Australian resident or citizen.

A spouse/de-facto is defined as a person of any gender who:

- Is in a legally recognised marriage, or

- Lives with you on a genuine domestic basis as a couple.

This means if you move in with your partner and they are an Australian resident; you may become liable for tax on worldwide income.

What about overseas investments such as shares or property?

- Personally owned overseas assets: If you own overseas investments — such as foreign shares or overseas investment properties — in your own name and remain a temporary resident (Subclass 444 with no Australian spouse), capital gains from selling these assets are generally not taxable in Australia.

- Assets sold by an Australian resident trust: If an Australian resident trust sells overseas shares or an overseas property and the gain is foreign-sourced, it is generally non-assessable, non-exempt income for a temporary resident beneficiary under s 768-910 ITAA 1997. Certain exceptions may still apply, such as where the gain relates to Australian employment income or where anti-avoidance provisions are triggered.

When Australian residents (for tax purposes) sell property valued at $750,000 or more and don’t provide a clearance certificate by settlement, 12.5% of the property purchase price must be withheld by the purchaser and paid to the ATO. This is known as the Foreign Resident Capital Gains Withholding (FRCGW) amount.

To avoid this withholding, Australian residents must obtain a ‘clearance certificate’ to prove they are not foreign residents. It is the vendor’s responsibility to secure the clearance certificate and provide it to the purchaser at or before settlement. To prevent any unforeseen delays and ensure the certificate is valid when presented to the purchaser, vendors should apply for the clearance certificate through the online form as early as possible in the sale process.

The main reasons a clearance certificate hasn’t been obtained before the settlement date are because clients:

- Don’t allow enough time to make an application before settlement (the standard processing time is 28 days).

- Have tax records that aren’t up to date.

- Haven’t needed to lodge tax returns for several years (e.g., when returns were not necessary).

If this happens to you, you must lodge a tax return to claim the credit that was withheld, even if your income is below the threshold to lodge. Obtain the ‘payment confirmation’ from the purchaser. When completing the tax return, be sure to:

- Declare your Australian assessable income, including any capital gain or loss from the disposal of the asset.

- Claim a ‘Credit for foreign resident capital gains withholding amounts’ taken from the sale proceeds.

The withheld amount will be refunded in full if:

- There are no tax debts.

- There’s no CGT payable on the sale of the property.

No, you cannot claim a full Capital Gains Tax (CGT) exemption if you purchase a home with an existing lease agreement. Your primary residence is typically exempt from capital gains tax (CGT). For CGT purposes, this exemption applies from the time you acquire your home, as long as you move in as soon as practicable.

There are specific circumstances that can affect when your property qualifies as your main residence for CGT purposes:

- Delays Due to Illness or Unforeseen Circumstances: If moving in is delayed due to illness or other unexpected events, your home remains exempt from CGT, provided you move in as soon as the cause of the delay is resolved (e.g., upon recovery from illness).

- Property Rented to Someone Else: If you cannot move in immediately because the property is rented out, it will not be considered your main residence until you actually move in.

- Owning Two Homes: If you buy a new home before selling your old one, you can designate both properties as your main residence for up to 6 months.

Example:

Emily signed a contract to buy a house in February. She took possession when settlement occurred in March.

We have provided two different scenarios below to explain what is considered practicable after settlement.

Scenario 1: Moving in as soon as practicable due to interstate work assignment

In early March, Emily’s employer assigned her to an interstate project for 5 months. She moved into the house when she returned in August.

Emily’s interstate assignment was unforeseen at the time she bought the house. She moved in as soon as practicable after the settlement of the contract. Therefore, she can treat the house as her main residence from the date she acquired it.

Scenario 2: Not practicable due to tenancy agreement

Alternatively, the house had an existing tenancy agreement that would not end until September, 6 months after the settlement. Due to this tenancy agreement, Emily could not move into the house until the lease ended in September.

In this case, Emily cannot treat the house as her main residence until she moves in. The property will only be exempt from CGT from the time she actually moves in, as it was not practicable for her to move in due to the existing tenancy agreement.

For Capital Gains Tax (CGT) purposes, your home qualifies for the main residence exemption from the time you acquire it, provided you move in as soon as practicable.

If you acquire a new home before you dispose of your old one, you can treat both properties as your main residence for up to 6 months under certain conditions.

You can claim this exemption if all of the following are true:

- You lived in your old home as your main residence for a continuous period of at least 3 months in the 12 months before you disposed of it.

- You did not use your old home to produce income (such as rent) during any part of that 12 months when it was not your main residence.

- The new property becomes your main residence.

If it takes longer than 6 months to dispose of your old home, the main residence exemption applies to both homes only for the last 6 months before you dispose of your old home. For the period before this, when you owned both homes, you can choose which home to treat as your main residence. The other property will be subject to CGT for that period.

Reference :

ATO – Moving to a new main residence

Transferring 50% Property: Navigate Capital Gian Tax Impact

When you sell, transfer, or gift a portion of your investment property to your spouse or partner, you are subject to capital gains tax. However, an exception exists: if the transfer involves your Principal Place of Residence (PPOR), you are exempt from capital gains tax obligations.

Empty Home Revival: Selling After 6 Years – Unleash CGT

If you are not treating any other property as your Principal Place of Residence (PPOR), you can continue to treat this property as your primary residence indefinitely after you have stopped residing in it.

Empower Your Quest: CGT Concession in Small Business

You are considered a CGT Concession Stakeholder in a company or trust if you are:

- A significant individual in that company or trust.

- The spouse of a significant individual and have a small but more than zero percent stake in the company or trust.

You can own this stake either directly or through other entities. To calculate your stake, use the same method as the significant individual test.

You’re a significant individual in a company or trust if you own at least 20% of it. This 20% can include both your direct ownership and indirect ownership through other entities.

Special Note – A spouse of a significant individual must have a participation percentage greater than zero in the business entity.

Small Business CGT Concession and Roll-Over Rules:

CGT Event J5 occurs if, after choosing a roll-over for a capital gain, you haven’t acquired a new asset or improved an existing one by the end of the allotted time. Additionally, this event happens if:

- The new or improved asset isn’t actively used in your business anymore (like if you’ve sold it, it’s now part of your trading stock, or it’s no longer used in your business operations).

- If the new asset is a share in a company or a trust interest, and it fails the 80% test (unless this failure is only temporary).

- You or a related entity aren’t significant stakeholders in the company or trust.

- The stakeholders in the company or trust don’t have a significant (at least 90%) investment in your business. When CGT Event J5 happens, you’ll have to recognize a capital gain. This is the same amount you initially didn’t have to pay tax on because of the small business roll-over. The capital gain is counted at the end of the time you were supposed to get or improve the asset.

Example: CGT event J5

In September 2020, Luke made a capital gain of $80,000 on an active asset. He met the maximum net asset value test.

Luke disregarded the whole capital gain under the small business roll-over.

In September 2022 (the end of the 2-year period), Luke did not have any replacement or capital improved assets. CGT event J5 happens, and Luke makes a capital gain of $80,000 in September 2022.

Source – ATO/ Small Business Rollover

While you can technically sell a property for $1, several crucial considerations apply. Tax authorities and legal entities typically assess property transactions based on market value, potentially resulting in tax obligations based on the property’s actual worth, despite the nominal sale price. Stamp duty, capital gains tax, and legal and financial implications, particularly if there are existing mortgages or loans, should be thoroughly evaluated.

Yes, Investax accountants are well-versed in CGT calculations. We can help you accurately determine your capital gain by considering various factors, such as the purchase price, sale price, holding period, and eligible deductions.

Capital gains in Australia are subject to taxation under the Capital Gains Tax (CGT) regime. If you’ve owned the asset for over 12 months, you may qualify for a 50% CGT discount on the gain, with the remaining 50% added to your taxable income and taxed at your marginal rate. Capital losses from other investments can offset capital gains, and any excess losses can be carried forward. There are exemptions for primary residences, concessions for small businesses, and different tax rates for superannuation funds. For accurate guidance in navigating the complexities of CGT, it’s advisable to consult a tax professional or accountant, such as Investax Accountants, as tax laws may change over time.

Capital gain is the financial profit realised when you sell or dispose of an asset, such as stocks, real estate, or valuable possessions, for an amount higher than the original purchase price. It represents the difference between the selling price (proceeds) and the cost basis (purchase price and any associated acquisition costs).

CGT is a tax on the profit made from the sale of an asset, including investment properties. If you sell an investment property for more than you paid for it, you may be subject to CGT. However, there are concessions and strategies available to minimize CGT, such as the 50% CGT discount for assets held longer than 12 months and the main residence exemption if the property was your main home for part of the time.

The rule that a company must have a public officer doesn’t come from the main company law, which is the Corporations Act 2001. Instead, it’s a tax rule. According to Section 252 of the Income Tax Assessment Act 1936, every company that does business in Australia or makes money from property in Australia needs to have a public officer. This public officer represents the company for all tax-related matters. The company itself, or someone with the proper authority from the company, must appoint this public officer.

a company is not required to have a secretary, but it if it does, then that secretary (or at least one of them if there is more than one secretary) must ordinarily be a resident of Australia. Refer S.204A.

No. At least ONE director has to be resident in Australia. Refer S.201A of the Corporations Act 2001.

A Director ID Number is a unique number given to an existing or intending director who has verified their identity with the Registrar. It is available via the Australian Business Registry Services (ABRS) website.

- A director ID is issued to a person forever.

- A person will keep their director ID even if they stop being a company director, change their name or move interstate or overseas.

- Director ID is being introduced to provide traceability of a director’s relationships over time, and across companies, to assist regulators and external administrators to investigate a director’s involvement in what may be repeated unlawful activity, including illegal phoenix activity.

- Both existing and new directors will need to apply.

Purchasing property through a company can provide limited liability, protecting your personal assets from the property’s debts or legal issues.

With the Labor government securing a strong election win, it’s highly likely the Division 296 tax will be reintroduced and passed—especially if the Greens support the bill in the Senate.

Under the current draft legislation, from 1 July 2025, individuals with a Total Superannuation Balance (TSB) exceeding $3 million will face an additional 15% tax on a portion of their superannuation earnings—including unrealised gains.

What’s changing?

If your TSB is over $3 million, a portion of your super earnings will be taxed at a higher effective rate of up to 30%—15% concessional tax (as usual), plus another 15% Division 296 tax on the proportion of earnings tied to the excess amount over $3 million.

This tax applies directly to you as an individual, not to your super fund. It will be calculated annually by the ATO, and you’ll have the option to pay it from your superannuation (even if you haven’t met a condition of release) or from personal funds.

Why is this controversial?

One major issue is that Division 296 tax includes unrealised gains—increases in the market value of your assets that you haven’t sold or received cash for. In simple terms, your super fund could be taxed simply because your investment property or shares increased in value on paper. This poses serious cash flow risks for SMSFs, especially those holding illiquid assets like real estate.

Is this just for the wealthy?

The government argues the tax will only affect the wealthiest 0.5% of super fund members (around 80,000 people in 2025–26). But there’s a catch: the $3 million threshold is not indexed to inflation. Over time, more Australians could be impacted, especially those making long-term contributions to SMSFs or holding appreciating assets.

Key Takeaways:

- Starts from 1 July 2025 if the bill pass.

- Applies only if your TSB exceeds $3 million at financial year-end.

- Taxed on a proportion of total earnings, including unrealised gains.

- The tax is personal—not levied on the fund.

- No indexation means the $3M threshold may impact more people over time.

- Cash flow planning will be critical for affected SMSFs.

It depends on the facts and the pattern of behaviour.

Division 7A allows a company loan to be repaid before the company’s tax return due date to avoid a deemed dividend. However, the tax law includes anti-avoidance rules that allow the ATO to ignore a repayment where it is not genuinely reducing the loan on a lasting basis.

These rules, set out in section 109R of the Income Tax Assessment Act 1936, are intention-based. Importantly, intention is not determined by what a taxpayer says, but by what a reasonable person would conclude from the surrounding facts and behaviour.

In practice, the ATO does not usually form a view based on a single isolated transaction. Instead, concern typically arises where there is a repeated pattern — for example, where loans are repaid shortly before year end and similar amounts are withdrawn again soon after, year after year. Over time, this pattern can indicate that repayments are only temporary and that company funds are being recycled.

Where such a pattern exists, the ATO may disregard the repayments, treat the loans as still outstanding, and apply Division 7A, potentially resulting in taxable deemed dividends.

That said, even a one-off arrangement can still fall within these rules if the surrounding circumstances clearly point to an intention to repay and re-borrow, particularly where the repayment is funded by further company loans.

Only where a loan is genuinely repaid, not effectively recycled, and does not fall within Division 7A would fringe benefits tax then be considered — and only if the loan arises from an employment relationship rather than share ownership.

In simple terms: The risk is not a single transaction in isolation, but a repeated pattern that shows company money is being temporarily “parked” to avoid tax.

For comprehensive information and expert guidance on Division 7A, we recommend reaching out to Investax accountants. We specialise in taxation matters and can provide you with the most up-to-date and tailored advice to ensure compliance with Division 7A rules. You can also visit the Australian Taxation Office (ATO) website for additional resources and information, but consulting with an Investax accountant can offer you personalised guidance specific to your situation.

To avoid Division 7A implications, private companies should ensure that loans and financial arrangements with shareholders or associates are structured in accordance with the Div 7A loan requirements. You can take out dividends and wages to avoid Div 7A Loan.

A Division 7A loan refers to a loan or financial arrangement made by a private company to a shareholder or their associate, where the terms and conditions of the loan are not at arm’s length or are less favourable than what would be available in a commercial transaction. Such loans are subject to Division 7A rules.

In Australia, many workers in industries such as mining, oil and gas, construction, and large infrastructure projects operate under FIFO (fly-in fly-out) arrangements. Under this setup, employees travel to remote job sites for rostered periods and stay there temporarily, while maintaining their usual home in another location—often in a major city.

Because FIFO workers are required to live away from their normal residence for work, employers may provide a living away from home allowance (LAFHA) to help cover additional accommodation and food costs. However, for the employer to access concessional fringe benefits tax treatment on this allowance, strict compliance requirements must be met—and one of the key requirements is obtaining a LAFHA declaration from the employee.

A FIFO LAFHA declaration is a formal statement confirming important details such as the employee’s normal place of residence, the temporary location they are staying in for work, and the period during which they are living away from home. This declaration supports the position that the employee is genuinely living away from home on a temporary basis, rather than relocating permanently.

If this declaration is not obtained, the employer may not be able to apply the available exemptions, which could result in the full allowance being subject to fringe benefits tax. For this reason, while it may seem like a simple form, the LAFHA declaration is a critical document to ensure the FIFO arrangement remains compliant and tax-effective for both the employer and the employee.

When deciding whether to buy a vehicle with finance or cash, the best option depends on your business structure, cash flow, and long-term tax planning goals.

Paying cash means you own the vehicle outright from day one, avoiding interest and loan commitments. It’s simple, cost-effective, and there’s no ongoing liability. However, it also ties up valuable capital that could otherwise be used for business growth or investment. If the vehicle is used for business purposes, you can generally claim tax deductions for depreciation and running costs—but not for interest, since no finance is involved.

Financing the vehicle—through a chattel mortgage or hire purchase—can provide flexibility and potential tax benefits. The interest and depreciation (or instant asset write-off, if eligible) are generally tax-deductible based on the business-use percentage. It also helps preserve cash flow by spreading the cost over time. However, many finance agreements include a balloon payment at the end of the term. While this reduces monthly repayments, it can create significant cash-flow pressure later if you decide to keep the vehicle instead of trading it in or refinancing.

A novated lease is another popular option—especially for employees who use their car for both business and personal use. Under a novated lease, your employer makes the lease payments from your pre-tax income, reducing your taxable income and simplifying running costs such as fuel, insurance, and maintenance. Similar to hire purchase agreements, novated leases often include a residual or balloon payment at the end of the term. While this lowers initial repayments, it can lead to a substantial cash-flow hit when you choose to retain the vehicle.

Ultimately, there’s no universal answer. If your business values liquidity and you want to maximise deductions through financing, a chattel mortgage or novated lease might be ideal. But if you prefer simplicity and full ownership without long-term obligations, paying cash could be the smarter move.

Tip: Before deciding, consult your Investax tax advisor to assess how each option affects your cash flow, Fringe Benefits Tax (FBT) exposure, and your broader business tax position.

Yes, you can generally continue to claim a tax deduction for the interest even after converting a variable loan to a fixed loan—provided the purpose of the loan remains income-producing.

The key factor the ATO looks at is what the loan is used for, not whether it’s fixed or variable. If the loan was originally taken out to acquire an investment property, shares, or any other income-generating asset, the interest on that loan remains deductible—even if you change the loan type.

It’s important to understand that deductibility follows the purpose, not the loan structure.

That said, here are a few considerations:

- Redrawing for personal use: If you redraw from the loan for private expenses (like buying a car or funding a holiday), the interest relating to that portion will no longer be deductible.

- Splitting loans: When refinancing, it’s wise to split loans to clearly separate investment and personal components, which makes recordkeeping and deductibility much simpler.

- Break costs: If you break a fixed loan early (to lock in a new rate or refinance again), you may incur break fees. These are not immediately deductible, but they may be amortised over five years or the remaining term of the loan—whichever is shorter.

So, in short, yes—switching from a variable to a fixed loan doesn’t affect your interest deduction as long as the loan is still for an income-producing purpose. Just make sure it’s structured right and keep good records.

If you’re refinancing or considering loan changes, it’s a good idea to check in with your accountant or tax adviser to ensure you’re not unintentionally affecting your deductions.

No, you cannot increase your tax-deductible loan by using equity from your investment property to reduce your home loan. This is because you are essentially swapping security rather than creating a new deductible loan. The ATO determines tax deductibility based on the purpose of the borrowed funds, and repaying a home loan is considered a private expense.

Example:

Let’s say you own Property A, which is an investment property, and Property B, which is your home. You decide to refinance Property A to access equity and use those funds to pay down the mortgage on Property B. While the new loan on Property A is secured against an investment property, the funds are being used for a private purpose (paying off your home loan). Because of this, the interest on the refinanced loan would not be tax-deductible.

If you are considering refinancing or restructuring your loans, we recommend seeking professional advice from Investax Property Tax Specilists to ensure you maximise tax benefits while staying compliant with ATO regulations. Feel free to reach out to us for guidance.

Lenders Mortgage Insurance (LMI) is a one-off, non-refundable, and non-transferable premium added to your home loan. It is calculated based on the size of your deposit and the amount you borrow. The larger your contribution to the purchase price of your property, the lower the LMI cost will be.

Here are some key points about LMI:

- LMI is typically required if you borrow more than 80% of your home’s value.

- The insurance is designed to protect the lender, not the borrower.

- Arranging LMI is not your responsibility; your lender will handle it for you.

- Increasing your deposit can significantly reduce or even eliminate the need for LMI.

Refinancing:

Refinancing is the process of replacing an existing loan with a new one, typically to secure better terms or lower interest rates. You should consider refinancing when interest rates drop significantly, as it can potentially reduce your monthly payments, save money on interest over the life of the loan, or shorten the loan term to pay off debt faster. Additionally, refinancing may make sense if your credit score has improved since you originally obtained the loan, as this can lead to more favourable terms. However, it’s essential to weigh the costs associated with refinancing, including application fees, and closing costs, against the potential benefits to determine if it’s a financially sound decision.

To increase your likelihood of loan approval:

- Maintain a good credit score by making timely payments.

- Reduce existing debt and manage credit responsibly.

- Save for a down payment or collateral, if required.

- Provide accurate and complete financial documentation.

- Shop around for lenders and loan options.

- Consider a co-signer if your credit is weak.

- Address any discrepancies or issues on your credit report.

- Demonstrate a stable income and employment history.

Credit score:

A credit score is a numerical representation of your creditworthiness. It’s calculated based on your credit history, including factors like your payment history, credit utilisation, length of credit history, and more. Lenders use your credit score to assess the risk of lending to you. A higher credit score typically means better loan terms and lower interest rates, while a lower score might result in less favourable terms or loan denials. It’s crucial to monitor and maintain a good credit score to access affordable loans and financial opportunities.

Difference between fixed-rate and variable-rate loans:

Fixed-rate loans have a constant interest rate throughout the loan term, providing predictable monthly payments. Variable-rate loans, also known as adjustable-rate loans, have interest rates that can change periodically, typically tied to a benchmark index. Fixed-rate loans offer stability, while variable-rate loans may start with lower rates but come with the risk of higher payments if rates rise. The choice depends on your risk tolerance and market conditions

Why Choose a Mortgage Broker Over a Bank Loan?

You might opt to engage a mortgage broker rather than approaching a bank directly because brokers offer several valuable benefits. These independent professionals have access to numerous lenders and loan products, including those from banks, potentially providing you with more favourable terms and rates. Mortgage brokers simplify the loan shopping process, saving you time and effort by researching and comparing various lender offers. They also offer expert advice tailored to your financial situation and goals, helping you navigate complex mortgage terms and conditions. Additionally, brokers may negotiate with lenders on your behalf to secure better terms and can be particularly helpful if you have unique financial circumstances or credit challenges. Their flexibility and convenience in scheduling meetings make the application process smoother. While banks are a valid option, working with a mortgage broker can enhance your choices and provide expert guidance to find the best mortgage for your specific needs.

Refinancing is the process of replacing an existing loan with a new one, typically to secure better terms or lower interest rates. You should consider refinancing when interest rates drop significantly, as it can potentially reduce your monthly payments, save money on interest over the life of the loan, or shorten the loan term to pay off debt faster. Additionally, refinancing may make sense if your credit score has improved since you originally obtained the loan, as this can lead to more favourable terms. However, it’s essential to weigh the costs associated with refinancing, including application fees, and closing costs, against the potential benefits to determine if it’s a financially sound decision.

- To increase your likelihood of loan approval:

- Maintain a good credit score by making timely payments.

- Reduce existing debt and manage credit responsibly.

- Save for a down payment or collateral, if required.

- Provide accurate and complete financial documentation.

- Shop around for lenders and loan options.

- Consider a co-signer if your credit is weak.

- Address any discrepancies or issues on your credit report.

- Demonstrate a stable income and employment history.

A credit score is a numerical representation of your creditworthiness. It’s calculated based on your credit history, including factors like your payment history, credit utilisation, length of credit history, and more. Lenders use your credit score to assess the risk of lending to you. A higher credit score typically means better loan terms and lower interest rates, while a lower score might result in less favourable terms or loan denials. It’s crucial to monitor and maintain a good credit score to access affordable loans and financial opportunities.

Fixed-rate loans have a constant interest rate throughout the loan term, providing predictable monthly payments. Variable-rate loans, also known as adjustable-rate loans, have interest rates that can change periodically, typically tied to a benchmark index. Fixed-rate loans offer stability, while variable-rate loans may start with lower rates but come with the risk of higher payments if rates rise. The choice depends on your risk tolerance and market conditions

You might opt to engage a mortgage broker rather than approaching a bank directly because brokers offer several valuable benefits. These independent professionals have access to numerous lenders and loan products, including those from banks, potentially providing you with more favourable terms and rates. Mortgage brokers simplify the loan shopping process, saving you time and effort by researching and comparing various lender offers. They also offer expert advice tailored to your financial situation and goals, helping you navigate complex mortgage terms and conditions. Additionally, brokers may negotiate with lenders on your behalf to secure better terms and can be particularly helpful if you have unique financial circumstances or credit challenges. Their flexibility and convenience in scheduling meetings make the application process smoother. While banks are a valid option, working with a mortgage broker can enhance your choices and provide expert guidance to find the best mortgage for your specific needs.

Yes, a foreign resident can contribute to their Australian superannuation fund and, in many cases, claim a tax deduction for it—provided specific conditions are met. Even if you’re living overseas, as long as you have assessable income in Australia and contribute to a complying Australian super fund, the contribution can generally be treated as tax deductible.

Here’s a simple example. Let’s say you’re a foreign resident who owns a rental property in Australia and earns $50,000 in annual rental income. Because you’re a non-resident, you’ll pay Australian tax on that $50,000 at the foreign resident tax rate. However, if you decide to contribute, for example, $10,000 of that income into your Australian super fund, and you submit a Notice of Intent to Claim a Deduction to your fund before lodging your tax return, this contribution can become tax deductible. In that case, your taxable income would reduce from $50,000 to $40,000—helping you save on tax while growing your retirement savings in a tax-effective way.

To be eligible, your super fund must be a complying fund and must accept personal contributions from non-residents. You’ll also need to submit a Notice of Intent to Claim a Deduction and receive acknowledgment from the fund confirming your notice before you lodge your tax return. It’s equally important to remember that deductions can only be claimed against your Australian-sourced income. If you have no income taxable in Australia—for example, if all your earnings are from overseas—then the deduction won’t provide any practical tax benefit, even though the contribution itself may still be allowed.

So, in summary, yes—you can contribute to your Australian super fund as a foreign resident, and if you have Australian income, those contributions can reduce your tax payable while helping you build long-term wealth for retirement. It’s a great way to turn Australian rental or investment income into future savings, provided you follow the correct process and meet the ATO’s requirements.

If you are a New Zealand citizen living in Australia on a Subclass 444 Special Category Visa, you are generally classed as a “temporary resident” for tax purposes — even though you may also be considered an Australian resident for tax purposes.

Under the ATO’s temporary resident rules, you only pay tax in Australia on your Australian-sourced income, such as:

- Salary or wages earned in Australia

- Rental income from Australian property

- Dividends from Australian shares

You do not pay tax on most foreign-sourced income or capital gains (for example, from overseas property or foreign shares), provided you:

- Hold a Subclass 444 visa, and

- Do not have an Australian citizen or permanent resident spouse/de-facto partner.

When could you lose your temporary resident status for tax purposes?

The ATO may revoke your temporary resident classification if you are in a spousal or de-facto relationship with an Australian resident or citizen.

A spouse/de-facto is defined as a person of any gender who:

- Is in a legally recognised marriage, or

- Lives with you on a genuine domestic basis as a couple.

This means if you move in with your partner and they are an Australian resident; you may become liable for tax on worldwide income.

What about overseas investments such as shares or property?

- Personally owned overseas assets: If you own overseas investments — such as foreign shares or overseas investment properties — in your own name and remain a temporary resident (Subclass 444 with no Australian spouse), capital gains from selling these assets are generally not taxable in Australia.

- Assets sold by an Australian resident trust: If an Australian resident trust sells overseas shares or an overseas property and the gain is foreign-sourced, it is generally non-assessable, non-exempt income for a temporary resident beneficiary under s 768-910 ITAA 1997. Certain exceptions may still apply, such as where the gain relates to Australian employment income or where anti-avoidance provisions are triggered.

If you are a foreign property owner in Australia, you are required to lodge a vacancy fee return for your residential property. It must be lodged annually within 30 days after the end of each vacancy year. This obligation applies to foreign investors who applied for property ownership after 9 May 2017 or purchased under a new or near-new dwelling exemption certificate. A foreign owner must lodge the return regardless of whether the property was occupied or rented.

A vacancy year is a 12-month period starting from the occupation day of the property, which is typically the settlement day for an established property or the day a certificate of occupancy is issued for a new one.

The vacancy fee applies if the property is not residentially occupied for at least 183 days or six months in a 12-month period. To be considered occupied, the dwelling must be either lived in by the owner or a relative, leased for a minimum of 30 days at a time, or genuinely available on the rental market at market rent. Short-term rentals (less than 30 days) do not count towards the 183-day requirement. If the return is not lodged on time, a vacancy fee may still apply, even if the property was occupied.

From 9 April 2024, the vacancy fee will be double the original foreign investment application fee. Some exemptions exist, such as if the property was undergoing substantial repairs, deemed unsafe, or if the owner was receiving long-term medical care. Owners must keep records for at least five years and update details if their foreign ownership status changes. Failure to comply can result in civil penalties or infringement notices from the Australian Taxation Office (ATO).

Australian citizens living abroad (expats) are not considered foreign owners, so they are not required to lodge a vacancy fee return.

Permanent residents (PRs) and New Zealand citizens with a Special Category Visa (Subclass 444) are also not classified as foreign owners, meaning they do not need to pay the vacancy fee.

Yes, even though you may not have permanent residency or citizenship in Australia, you will still be treated as an Australian resident for tax purposes. Remember, tax residency differs from immigration residency, so don’t let this confuse you. If you are an Australian resident for tax purposes, you can claim the Tax-Free Threshold, which is $18,200. You are eligible to claim it from this payer if one of the following conditions applies:

- You are not currently claiming the tax-free threshold from another payer.

- You are already claiming the tax-free threshold from another payer, but your total income from all sources is expected to be less than $18,200.

The short answer is yes, but it comes with specific conditions. If you are an overseas student who has arrived in Australia to pursue your studies and are enrolled in a course that lasts more than 6 months, you are generally considered an Australian resident for tax purposes. This status affects how you are taxed and what you need to declare in your TFN declaration to your employer.

Yes, even though you may not have permanent residency or citizenship in Australia, you will still be treated as an Australian resident for tax purposes. Remember, tax residency differs from immigration residency, so don’t let this confuse you. If you are an Australian resident for tax purposes, you can claim the Tax-Free Threshold, which is $18,200. You are eligible to claim it from this payer if one of the following conditions applies:

- You are not currently claiming the tax-free threshold from another payer.

- You are already claiming the tax-free threshold from another payer, but your total income from all sources is expected to be less than $18,200.

The short answer is yes, but it comes with specific conditions. If you are an overseas student who has arrived in Australia to pursue your studies and are enrolled in a course that lasts more than 6 months, you are generally considered an Australian resident for tax purposes. This status affects how you are taxed and what you need to declare in your TFN declaration to your employer.

In Australia, many workers in industries such as mining, oil and gas, construction, and large infrastructure projects operate under FIFO (fly-in fly-out) arrangements. Under this setup, employees travel to remote job sites for rostered periods and stay there temporarily, while maintaining their usual home in another location—often in a major city.

Because FIFO workers are required to live away from their normal residence for work, employers may provide a living away from home allowance (LAFHA) to help cover additional accommodation and food costs. However, for the employer to access concessional fringe benefits tax treatment on this allowance, strict compliance requirements must be met—and one of the key requirements is obtaining a LAFHA declaration from the employee.

A FIFO LAFHA declaration is a formal statement confirming important details such as the employee’s normal place of residence, the temporary location they are staying in for work, and the period during which they are living away from home. This declaration supports the position that the employee is genuinely living away from home on a temporary basis, rather than relocating permanently.

If this declaration is not obtained, the employer may not be able to apply the available exemptions, which could result in the full allowance being subject to fringe benefits tax. For this reason, while it may seem like a simple form, the LAFHA declaration is a critical document to ensure the FIFO arrangement remains compliant and tax-effective for both the employer and the employee.

When deciding whether to buy a vehicle with finance or cash, the best option depends on your business structure, cash flow, and long-term tax planning goals.

Paying cash means you own the vehicle outright from day one, avoiding interest and loan commitments. It’s simple, cost-effective, and there’s no ongoing liability. However, it also ties up valuable capital that could otherwise be used for business growth or investment. If the vehicle is used for business purposes, you can generally claim tax deductions for depreciation and running costs—but not for interest, since no finance is involved.

Financing the vehicle—through a chattel mortgage or hire purchase—can provide flexibility and potential tax benefits. The interest and depreciation (or instant asset write-off, if eligible) are generally tax-deductible based on the business-use percentage. It also helps preserve cash flow by spreading the cost over time. However, many finance agreements include a balloon payment at the end of the term. While this reduces monthly repayments, it can create significant cash-flow pressure later if you decide to keep the vehicle instead of trading it in or refinancing.

A novated lease is another popular option—especially for employees who use their car for both business and personal use. Under a novated lease, your employer makes the lease payments from your pre-tax income, reducing your taxable income and simplifying running costs such as fuel, insurance, and maintenance. Similar to hire purchase agreements, novated leases often include a residual or balloon payment at the end of the term. While this lowers initial repayments, it can lead to a substantial cash-flow hit when you choose to retain the vehicle.

Ultimately, there’s no universal answer. If your business values liquidity and you want to maximise deductions through financing, a chattel mortgage or novated lease might be ideal. But if you prefer simplicity and full ownership without long-term obligations, paying cash could be the smarter move.

Tip: Before deciding, consult your Investax tax advisor to assess how each option affects your cash flow, Fringe Benefits Tax (FBT) exposure, and your broader business tax position.

Yes, you can purchase a car in the name of your trust. However, whether you can claim a tax deduction for it is not a straightforward answer. It depends on how the car is used and the nature of your trust’s activities.

What Does Your Trust Do?

🔹 Investment Trust (Property or Shares):

If your trust is primarily used for passive income activities, such as holding rental properties or shares, then there is no clear business connection to justify claiming tax deductions for the vehicle. In this case, the car is likely to be used for personal purposes, which means deductions are generally not allowed.

🔹 Active Business Trust:

If the trust actively operates a business—such as a consulting firm, construction company, or retail store—then there may be a valid business reason for purchasing the vehicle. In this case, tax deductions may be available, provided the car is genuinely used for business purposes.

Fringe Benefits Tax (FBT) Considerations

Owning a personal-use vehicle in a trust can sometimes create additional tax reporting requirements because Fringe Benefits Tax (FBT) may apply.

If the trust provides a car to a trustee, employee, or beneficiary for personal use, the trust may be liable for FBT. This tax applies when a vehicle is used for non-business purposes, and it can significantly impact the overall tax benefit.

This is an age-old question, and unfortunately, it doesn’t have a straightforward yes or no answer. Generally, novated leases are subject to Fringe Benefits Tax (FBT). When employers provide personal benefits like motor vehicles for personal use, gym memberships, holiday tours, etc., to their employees or their employees’ family members, these are considered fringe benefits. Employers then pay the top marginal tax rate (47%, which includes the 45% top tax rate plus the Medicare Levy of 2%) for these benefits.

Novated leases are often marketed as hassle-free, with claims that employees won’t have to worry about GST, running expenses, and can pay for the lease with post-tax income, as the employer handles the lease payments and FBT. However, complications can arise if you leave employment and are required to pay a significant amount to exit the lease. Additionally, if you wish to own the vehicle after the lease term, you may face a substantial balloon payment from your post-tax salary.

Employers often attempt to reduce FBT by using the Employee Contribution Method (ECM), where a portion of the lease is paid from the employee’s post-tax salary. If too much ECM is applied, the benefits of the lease may diminish, making it less attractive to employees.

For those planning to purchase an electric vehicle, a novated lease can be particularly beneficial, as employers are exempt from FBT, meaning no ECM calculation is required.

To determine if a novated lease is worthwhile for you, consult your accountant. If you don’t have a dedicated accountant, consider reaching out to Investax Tax Specialists for expert advice on these types of questions.

The goods and services tax (GST) does not apply to residential rents, so Airbnb hosts do not have to pay it. This also means that you can’t get a GST credit for the costs that go along with it. This is applied even if your sales are more than $75,000, which is the GST threshold.

Please check feel free to check out our Tax Consequence guide for Airbnb.

You can continue making super contributions after retirement, but the rules depend on your age, your total super balance (TSB), and whether concessional or non-concessional contributions are being made.

The work test only applies if you’re aged 67 to 74 and you want to claim a tax deduction for personal super contributions. If you’re under 67, or making non-concessional contributions, no work test is required.

- Personal Contributions (Tax Deduction): Yes, you can claim a tax deduction on a personal contribution as long as it doesn’t push you into a tax loss position. Generally tax accountants do not recommend claiming deductions when your taxable income is below the tax-free threshold of $22,575 for FY26, as there is usually no benefit in doing so.

- Catch-Up Contributions: Yes, catch-up concessional contributions are available if your total super balance (TSB) is under $500,000 on 30 June 2025, and you have unused concessional cap amounts from the past five years.

- Non-Concessional and Bring-Forward Contributions: Yes, you can make non-concessional contributions and use the bring-forward rule if your super balance is below the ATO thresholds. For FY26, the rules are:

-

- TSB less than $1.76 million → up to $360,000 (3-year bring-forward)

- TSB $1.76m – under $1.88m → up to $240,000 (2-year bring-forward)

- TSB $1.88m – under $2m → up to $120,000 (standard annual cap)

- TSB $2m or more → no non-concessional contributions allowed

If you need to travel far or to another city for work and stay overnight before starting your duties, you might wonder whether these costs are deductible. The general tax rule in Australia is that travel from home to your regular place of work is considered private and not deductible, even if it involves flying long distances or staying overnight.

For example, if your employer requires you to travel at your own expense to the same city every week and then provides transport to various worksites the following day, the initial flight and overnight accommodation are still regarded as private travel. These expenses are essentially about putting you in the position to start work, not costs incurred while doing your actual job.

The ATO explains this in TR 2021/1 Income tax: when are deductions allowed for employees’ transport expenses, which gives the example of an employee who regularly flies interstate for work. Even though she stays overnight, the costs are not deductible because they are related to her personal choice of where to live compared to where she works.

That said, there are limited circumstances where travel expenses may be deductible, such as:

- Co-existing workplaces – where you genuinely have two regular places of work (for example, one near home and another interstate).

- Special demands travel – where the employer directs you to travel, pays you for the travel time, and the travel is part of the job itself (not just getting to work).

In most cases, though, if the travel is simply to get closer to your normal workplace, the costs will not be deductible.

Key takeaway: If you are flying to the same city each time and staying overnight before going to work, these travel and accommodation expenses will usually be considered private and not deductible. To be deductible, the travel must be clearly linked to carrying out your work duties—not just getting to your workplace.

You may be wondering, are financial advice fees tax-deductible in Australia? The answer is yes — but only in certain situations. The ATO allows individual taxpayers to claim deductions for some types of financial advice fees, but there are strict limits. Importantly, the fees must be paid by you personally (not through your superannuation). Below is a breakdown of which financial advice fees you can and cannot claim as a tax deduction.

- Eligible Deductions (When You Can Claim)

You may claim deductions for financial advice fees you personally pay in the following circumstances:

- Ongoing advice fees for income-producing investments — for example, regular annual or semi-annual reviews of the performance of your investments.

- Fees for advice about your existing portfolio — such as whether the mix of your income-producing investments is still appropriate and whether to keep or sell those assets.

- Fees for advice on income protection insurance products.