Publish Date: May 28, 2024

Division 293 tax is an extra tax on superannuation contributions. It applies to people whose total income and super contributions add up to more than $250,000 in a year. This tax reduces the tax break they get on their super contributions by making them pay an additional 15% tax on top of the regular 15% tax that super contributions usually attract.

Division 293 tax is an extra 15% tax. It is applied to the smaller amount between the excess income over $250,000 and the taxable super contributions. Check Sarah’s example below for further explanation.

Your ‘Division 293 Notice of Assessment’ will only be sent to you once the ATO receives the contribution information from your super fund.

The income component of the Division 293 tax calculation is based on the same income calculation used to determine the Medicare levy surcharge (MLS), disregarding any reportable superannuation contributions. The components of this income calculation are:

- Taxable income (assessable income minus allowable deductions)

- Total reportable fringe benefits amount

- Net financial investment loss

- Net rental property loss

- Net amount on which family trust distribution tax has been paid

- Super lump sum taxed elements with a zero-tax rate

- Assessable first home super saver released amount

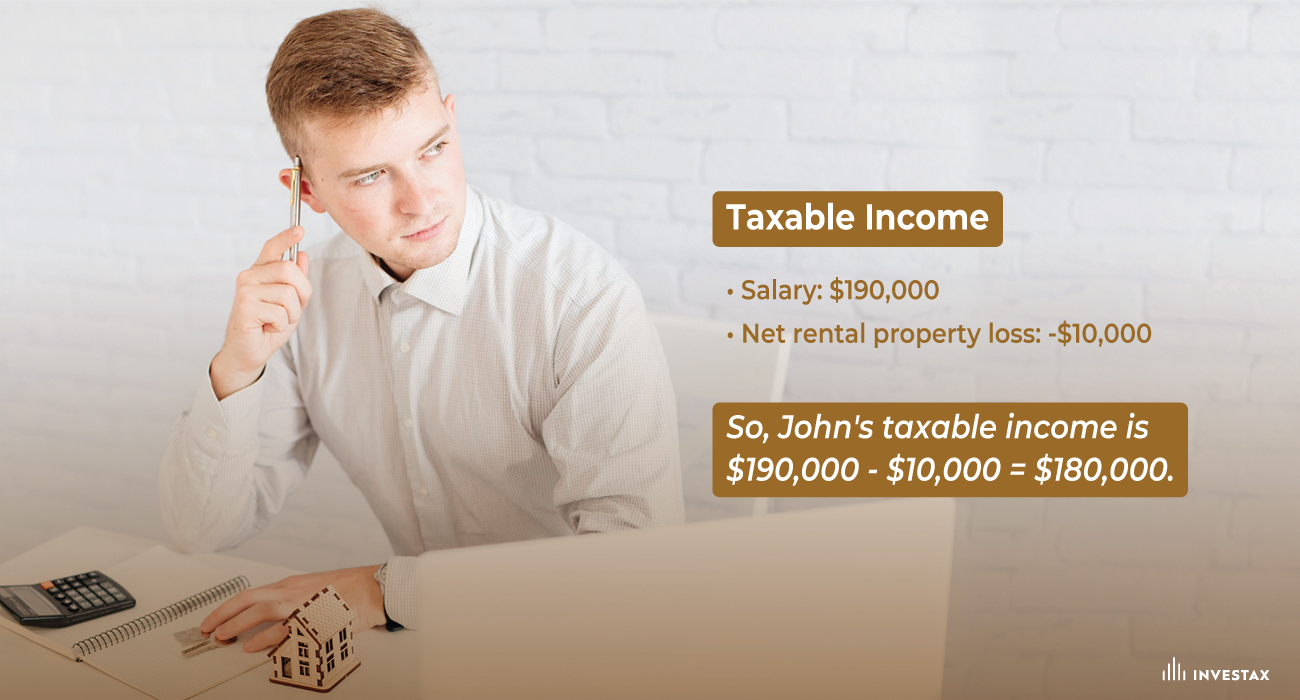

Example for John:

John earns a salary of $190,000, and his employer contributes $25,000 into superannuation for him. John also has a net rental property loss of $10,000.

Taxable Income:

- Salary: $190,000

- Net rental property loss: -$10,000

So, John’s taxable income is $190,000 – $10,000 = $180,000.

Division 293 Income:

- Taxable income: $180,000

- Net rental property loss: +$10,000

- Employer super contributions: +$25,000

John’s Division 293 income is $180,000 + $10,000 + $25,000 = $215,000, which is within the limit of $250,000. Therefore, John’s entire concessional contributions (CCs) would be taxed at 15%, and Division 293 tax does not apply.

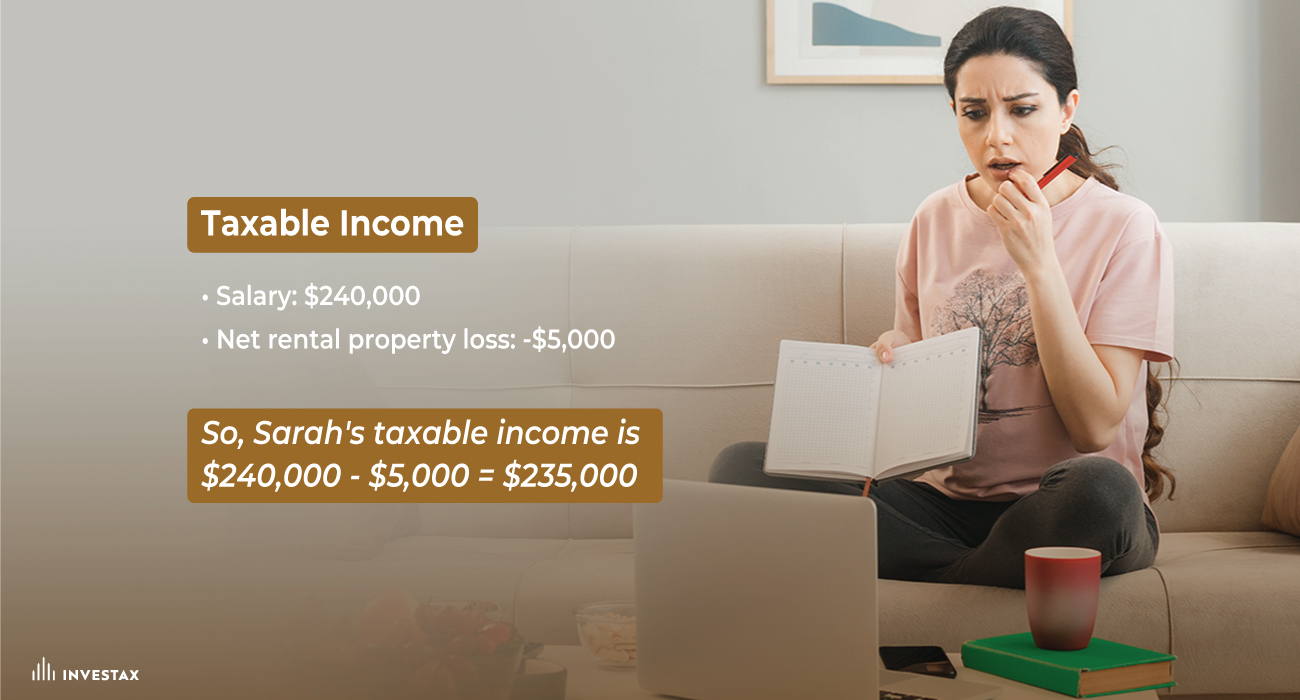

Example for Sarah:

Sarah earns a salary of $240,000, and her employer contributions for the year are $30,000. Sarah also has a net rental property loss of $5,000.

Taxable Income:

- Salary: $240,000

- Net rental property loss: -$5,000

So, Sarah’s taxable income is $240,000 – $5,000 = $235,000.

Division 293 Income:

- Taxable income: $235,000

- Net rental property loss: +$5,500

- Employer super contributions: +$27,500

So, Sarah’s Division 293 income is $235,000 + $5,500 + $27,500 = $268,000. Since Sarah’s income exceeds the threshold of $250,000, she will pay 15% contributions tax on her employer contributions and will also be liable for Division 293 tax. Division 293 taxable contributions are the lesser of Division 293 super contributions ($27,500) or the amount above the $250,000 threshold ($18,000). Sarah will pay additional 15% tax on $18,000.

She can choose to pay this tax personally, or she can choose to release the tax from her super fund.

ATO Reference – Div 293

General Advice Warning

The material on this page and on this website has been prepared for general information purposes only and not as specific advice to any particular person. Any advice contained on this page and on this website is General Advice and does not take into account any person’s particular investment objectives, financial situation and particular needs.

Before making an investment decision based on this advice you should consider, with or without the assistance of a securities adviser, whether it is appropriate to your particular investment needs, objectives and financial circumstances. In addition, the examples provided on this page and on this website are for illustrative purposes only.

Although every effort has been made to verify the accuracy of the information contained on this page and on our website, Investax Group, its officers, representatives, employees and agents disclaim all liability [except for any liability which by law cannot be excluded), for any error, inaccuracy in, or omission from the information contained in this website or any loss or damage suffered by any person directly or indirectly through relying on this information.