Overview

Many taxpayers use their primary residence for work or business purposes. A common concern is whether using the property in this way will affect their primary residence exemption. People often wonder, “Are we losing the primary residence exemption if we use the property for business purposes?” Another consideration is whether the property can be classified as an active asset for the portion used for business, thus allowing the claim of small business CGT concessions.

To address these concerns, we present the following private ruling as an example of how the tax office views using your primary residence for business purposes. Although private rulings are specific to individual circumstances, the underlying principles of the applicable laws are generally consistent.

If you find yourself in a similar situation and are unsure about the relevant laws, please feel free to contact Investax Group for personalized assistance.

Background

Case Year: 2024

Resident: John Doe

Property Purchase: February 2006

John Doe, an Australian resident for tax purposes, purchased a property in February 2006. The property consists of a dwelling and five small commercial shop outlets on a single lot of land, with a total area of less than 2 hectares. The dwelling occupies 80% of the land, while the shop outlets occupy under 20%.

Since acquiring the property, John has resided in the dwelling as his main residence and has not used it to produce income. From the financial years ending 2007 to 2021, John used one of the shop outlets to operate his business through a discretionary trust entity, with his spouse as the trustee and himself as a beneficiary. During these years, John actively worked full-time in the business. The remaining shop outlets were leased to unrelated entities.

More of the land was used for John’s business than for deriving rent during this period. However, on average, the business earned more income from rent than from business operations. In 2021, John’s business no longer required a physical premises, and all shop outlets were leased to unrelated entities. Now, John is preparing to sell the property.

Questions

1. Does the main residence exemption apply in accordance with section 118-100 of the ITAA 1997 where the land comprises of both main residence and commercial premises (shops)?

2. Can the land be deemed to be an active

Main Residence Exemption

The main residence exemption is a provision in Australian tax law that allows homeowners to be exempt from paying capital gains tax (CGT) on the sale of their primary residence. Under section 118-100 of the Income Tax Assessment Act 1997 (ITAA 1997), a property must be the taxpayer’s main residence to qualify for this exemption.

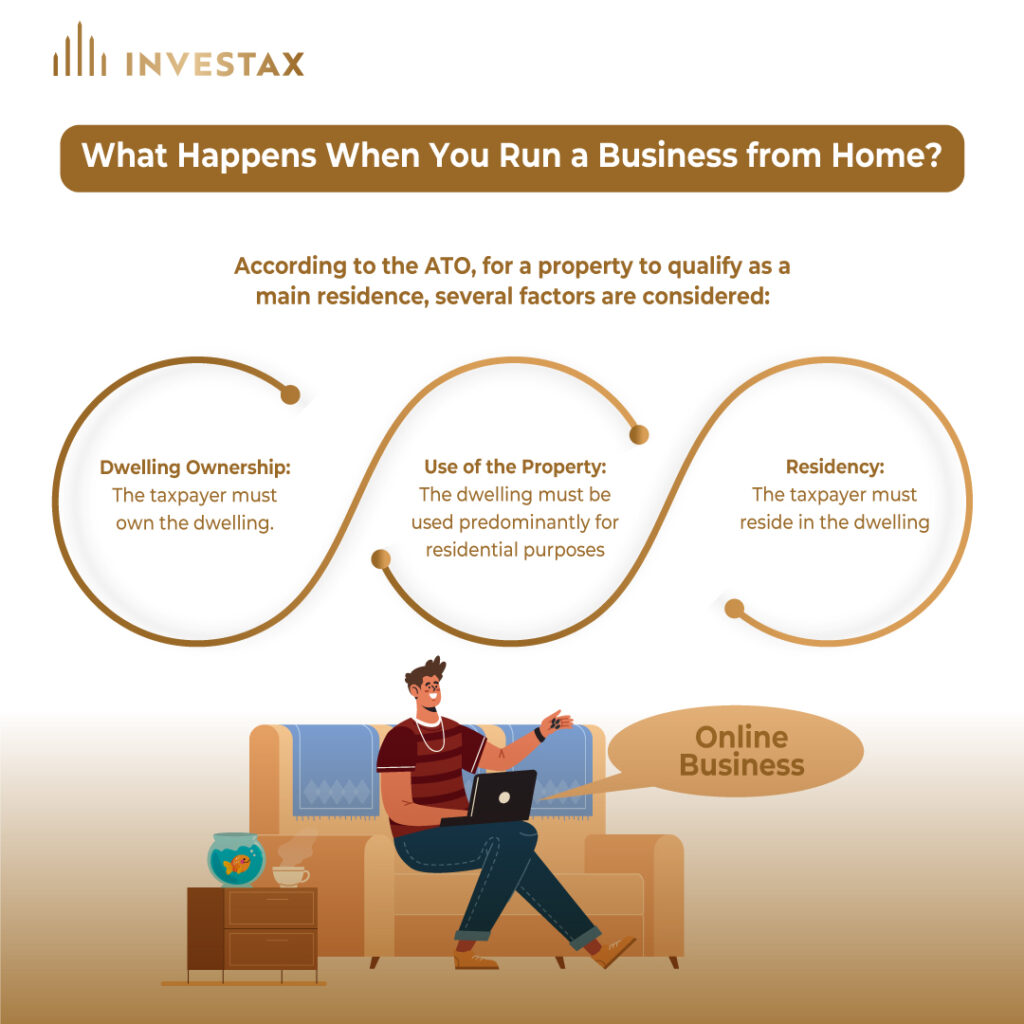

According to the ATO, for a property to qualify as a main residence, several factors are considered:

- Dwelling Ownership: The taxpayer must own the dwelling.

- Use of the Property: The dwelling must be used predominantly for residential purposes.

- Residency: The taxpayer must reside in the dwelling.

John has met all these criteria. Since the acquisition of the property, John has resided in the dwelling as his main residence and has not used it to produce income. The ATO confirmed that John used the dwelling as his main residence throughout his ownership period and did not use it to produce income. Therefore, he is entitled to the full main residence exemption on the disposal of the main residence.

To calculate the exempt portion, John needs to determine the proportion of the property used as his main residence. Since the dwelling occupies 80% of the land, he will calculate the CGT exemption based on this proportion.

Example Calculation:

Assume John sells the property for $1,000,000. The dwelling, which occupies 80% of the land, would be valued at $800,000. Therefore, the CGT exemption would apply to $800,000 of the sale proceeds, and John would need to consider CGT on the remaining $200,000.

Active Asset Classification

The active asset test, as outlined in section 152-35 of the ITAA 1997, is a crucial component for determining eligibility for small business CGT concessions. To be classified as an active asset, a property must meet specific requirements:

- Ownership Duration: The asset must be owned for more than 15 years. Or half of the test period if you have owned it for 15 years or less.

- Active Use: The asset must be an active asset for at least 7.5 years within the test period, which starts upon acquisition and ends at the CGT event.

An asset is considered active if it is used or held ready for use in the course of carrying on a business by the taxpayer, their affiliate, or a connected entity.

In John’s case, his business operated for over 7.5 years from 2007 to 2021. The property meets the active asset test as it was owned by John for more than 15 years and was an active asset for more than 7.5 years during this period. The ATO found that John used more of the non-residential land for business purposes than for deriving rent, satisfying the active asset criteria.

Example Calculation:

Assume the property was purchased for $500,000 in 2006 and is sold for $1,000,000 in 2024. The capital gain from the sale is $500,000. Since the property qualifies as an active asset, John can apply both the 50% Capital Gains Tax (CGT) discount and the 50% active asset reduction. This reduces the taxable gain to $125,000. Furthermore, John can potentially minimize the capital gain to zero by applying additional small business CGT concessions.

Conclusion

This case study, based on a private ruling, illustrates how the main residence exemption and active asset classification can apply to a property with mixed use. It highlights the importance of understanding the conditions under which these tax exemptions and classifications are granted by the ATO. John Doe’s situation demonstrates that a property used predominantly as a main residence, with portions used for business, can qualify for significant tax concessions when the relevant criteria are met.

For more detailed and official information, please refer to the ATO website or consult with a tax professional. Understanding these provisions can significantly impact financial planning and tax obligations for property owners in Australia. If you are unsure about your tax treatment or need personalized advice, we encourage you to reach out to Investax Group’s tax specialists for expert guidance.

Reference

ATO – Private Ruling

ATO – Active Asset

Glossary:

Discretionary Trust: A trust where the trustee has the discretion to decide which beneficiaries receive the income or capital from the trust and how much each is to receive. This is relevant in the case where John operated his business through a discretionary trust.

Dwelling: A building or part of a building that is used predominantly for residential accommodation. The term is crucial when determining eligibility for the main residence exemption.

Main Residence Exemption: A CGT exemption that allows homeowners to be exempt from paying tax on the sale of their main residence. To qualify, the property must be the taxpayer’s primary home and used predominantly for residential purposes.

Private Ruling: A written decision by the ATO that applies tax laws to a taxpayer’s specific circumstances. While rulings are tailored to individual cases, they provide insights into how the ATO interprets tax laws.

Small Business CGT Concessions: Tax concessions that allow small business owners to reduce or defer CGT on business assets. For instance, active asset classification can enable access to these concessions.

Trustee: An individual or organization responsible for managing a trust. In John’s case, his spouse acted as the trustee of the discretionary trust through which the business was operated.