The Retirement Tax Trap: How the New 30% CGT Floor Makes “Waiting Until Retirement to Sell” Strategy Obsolete

Bare Trust: A Complete Guide for SMSF Property Investors

|

|

June 4, 2025 |

Bare Trusts play a crucial role when purchasing property through a Self-Managed Super Fund (SMSF), especially when borrowing is involved. Many investors find the concept of a Bare Trust confusing, as it differs significantly from a discretionary or family trust in both purpose and structure.

This structure has become essential for investors looking to use their superannuation to purchase property while complying with strict super laws. Purchasing property through an SMSF using a Bare Trust allows investors to access opportunities for long-term capital growth and rental income, all while growing their retirement savings in a tax-advantaged environment. However, this strategy also introduces complexity and carries significant compliance obligations.

This guide aims to simplify the process and explain how Bare Trusts work within the SMSF framework.

What Is a Limited Recourse Borrowing Arrangement (LRBA)?

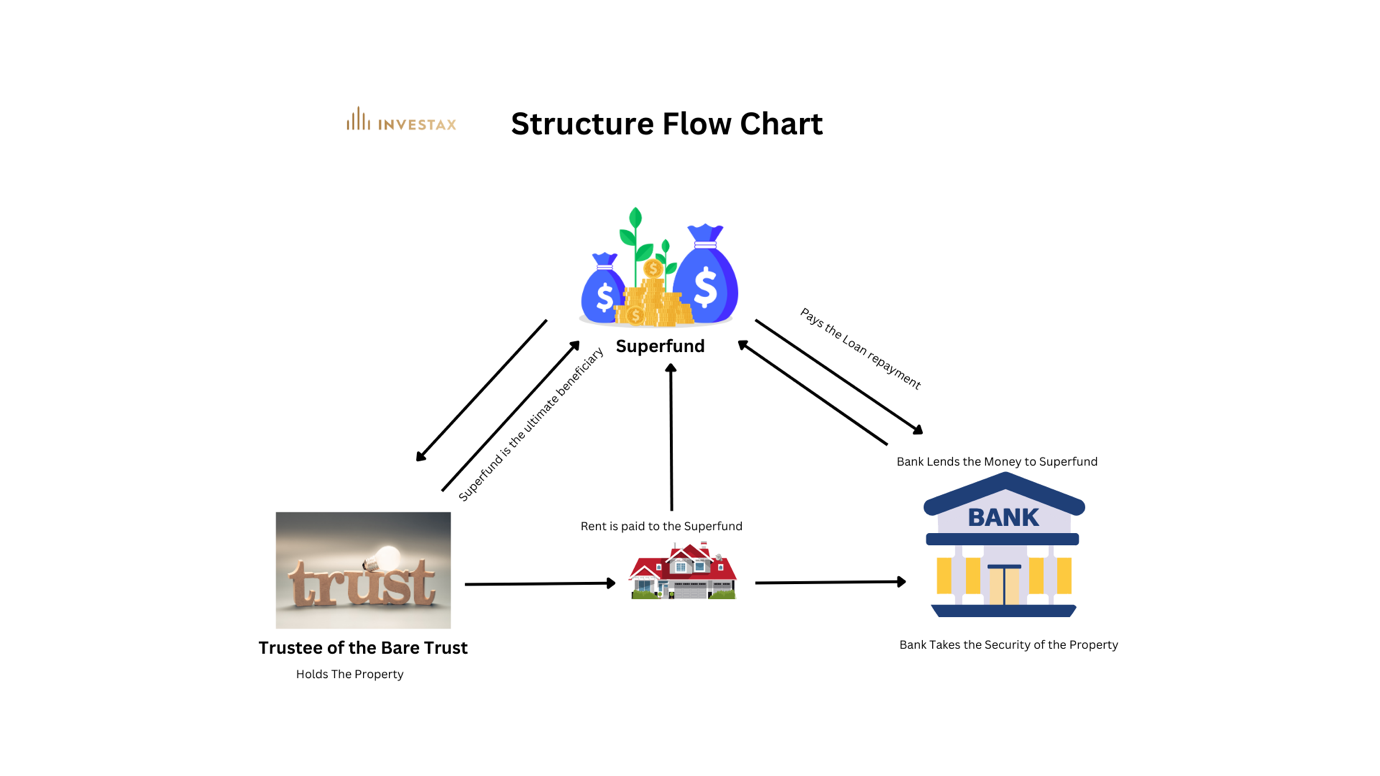

To understand a Bare Trust, you first need to understand a Limited Recourse Borrowing Arrangement (LRBA). In the world of SMSFs, these two structures go hand in hand—one cannot operate without the other when borrowing is involved. This type of loan allows you to purchase residential or commercial property, with the Super Fund covering the deposit and any other costs, such as stamp duty. It complies with Government Legislation (SIS Act – s67A, 67B). As a ‘Limited Recourse Loan,’ the lender can only claim the property held as security and cannot access any other Super Fund assets.

Before these amendments came into effect in 2007, SMSFs were not allowed to borrow money to purchase assets. Today, SMSFs can borrow under a Limited Recourse Borrowing Arrangement (LRBA), provided the loan is used to acquire a single acquirable asset, and the lender’s rights are limited to that asset alone. This means that if the SMSF defaults, the lender cannot access any other assets in the fund beyond the property used as loan security.

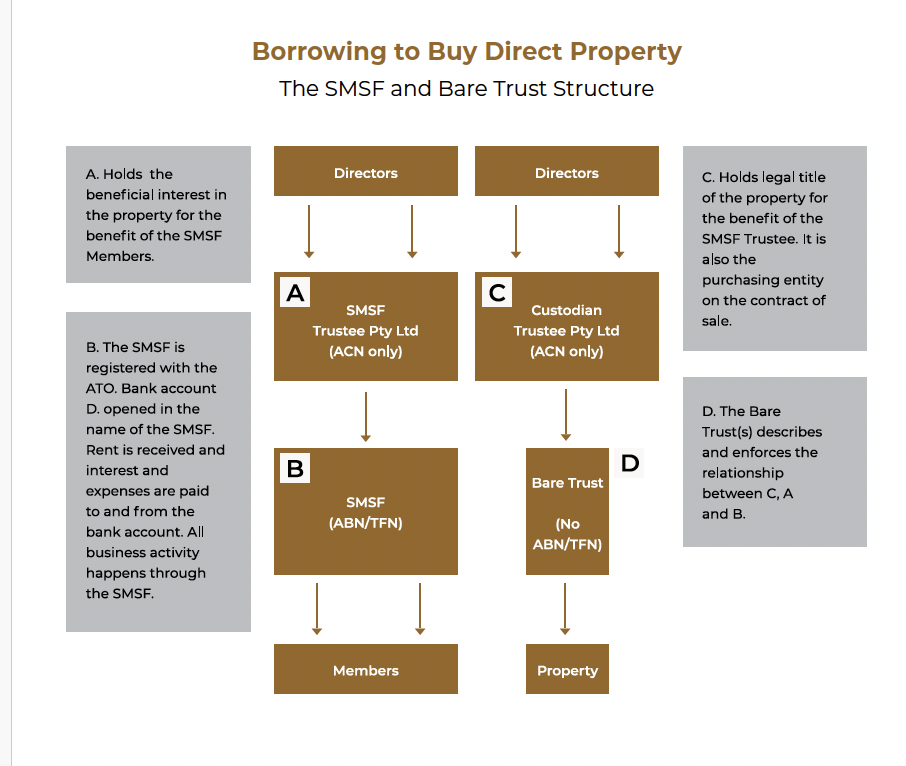

What Is a Bare Trust in an SMSF LRBA?

A Bare Trust, also known as a custodian trust, is a critical part of the structure when an SMSF borrows money under a Limited Recourse Borrowing Arrangement (LRBA). In this arrangement, the Bare Trustee holds the legal title to the property, while the SMSF holds the beneficial interest. The trust exists solely to hold the asset during the life of the loan and plays no active role in managing or controlling the property. The SMSF receives all rental income and bears all expenses. Once the loan is fully repaid, the legal title to the property can be transferred from the Bare Trust to the SMSF—often without incurring additional stamp duty, depending on state laws.

One of the most important documents in this process is the Property/Bare Trust Deed. It must be drafted with extreme care, as errors can lead to serious GST, stamp duty, or tax consequences. The SIS Act specifically requires that any asset purchased with borrowed funds “is held on trust” for the SMSF, which must be the beneficial owner at all times. A poorly prepared deed can jeopardise the entire arrangement or cause the fund to become non-compliant.

What Is a Single Acquirable Asset Under an LRBA?

When an SMSF uses a Limited Recourse Borrowing Arrangement (LRBA) to purchase property, there are strict rules that must be followed to ensure compliance with superannuation law. A Bare Trust is the legal mechanism that holds the property purchased under an LRBA, ensuring the fund remains compliant with superannuation laws.

The most important rule is that the SMSF can only borrow to acquire a single acquirable asset—typically one residential or commercial property held under a single legal title. If the property consists of multiple titles, it may no longer qualify under the LRBA rules.

For instance, if an SMSF wants to purchase a commercial unit with a separately titled car park, even though both are being sold together in one contract, they are treated as two separate assets. This would not meet the definition of a single acquirable asset unless both titles are consolidated prior to the purchase. Situations like these are commonly misunderstood, and failing to structure the purchase correctly could breach the borrowing rules.

You cannot buy a second property using the same Bare Trust, as each trust can only hold one single acquirable asset under LRBA rules. If your SMSF wants to purchase another property with a loan, a new Bare Trust must be set up for that separate purchase.

Note: The same trustee can be used for multiple Bare Trusts, but each property must have its own separate trust deed.

Who Borrows the Money from the Bank?

In an SMSF property purchase using a Limited Recourse Borrowing Arrangement (LRBA), it is the SMSF that borrows the money from the bank—not the Bare Trust. The SMSF is the borrower and is responsible for making all loan repayments, receiving rental income, and managing the property as the beneficial owner. The Bare Trust, also known as the custodian trust, merely holds the legal title to the property while the loan is in place. Although the SMSF is the borrower, many lenders require personal guarantees from the individual members of the fund to secure the loan. This structure ensures that the lender’s recourse remains limited to the property itself, while the SMSF retains full control over the investment and its income.

Note – for Designer – copy paste the this from – https://investax.com.au/insight/all-you-need-to-know-about-smsf-bare-trust-and-limited-recourse-borrowing/

Can You Refinance and Take Equity Out?

Yes, an SMSF can refinance an existing Limited Recourse Borrowing Arrangement (LRBA), but taking equity out—as you might in a personal or investment loan outside super—is not permitted under current superannuation laws. The refinance must be like-for-like, meaning the new loan can only cover the outstanding balance of the original borrowing or improve loan terms such as interest rate or repayment structure.

There are important loan restrictions when an SMSF uses a Bare Trust and Limited Recourse Borrowing Arrangement (LRBA) to buy property. Refinancing is allowed, but only under strict conditions—the new loan must be on the same terms or better than the original. You cannot increase the loan amount or access equity as you might with a regular investment loan.

In addition, one Bare Trust can only hold one standalone property, and no other assets inside or outside the SMSF can be used as security. The property must be complete at the time of purchase, meaning you can’t use borrowed funds to build, develop, or make major renovations. Similarly, vacant land cannot be purchased under an LRBA.

Who Signs the Contract of Sale When Purchasing a Property in a Bare Trust?

When a property is purchased using an SMSF with a loan, the Bare Trustee is the one who signs the Contract of Sale—not the SMSF itself. This is because the Bare Trustee holds the legal title to the property during the loan period, while the SMSF is the beneficial owner. It’s important that the contract is signed only in the name of the Bare Trustee, without mentioning the SMSF or the trust. For example, the buyer should be listed simply as “ABC Holdings Pty Ltd,” not “ABC Holding Pty Ltd as trustee for ABC Bare Trust.” Including the trust name can be seen as a separate declaration of trust and may lead to extra stamp duty.

The timing of when the Bare Trust Deed is signed also matters and varies between states. In Queensland, the deed must be signed before or on the same day as the contract. In New South Wales, it’s usually signed after the contract. Getting the sequence wrong can lead to compliance and tax issues, so it’s best to get professional advice to make sure everything is done correctly from the start.

Disclaimer: The rules and procedures can vary depending on your state or situation. Please check with your legal advisor before signing any contracts or setting up a Bare Trust.

Legal Ownership Requirements in Australia

Below is the current advice from the legal team at DOCSCENTRE in relation to names on the contract for each State when purchasing property via a LRBA arrangement in a super fund.

| State | Name of Purchaser | Date of Custodian Trust | Duty |

| Victoria | Custodian Trustee Pty Ltd (name and ACN) | After the date of the contract | Nil |

| New South Wales | Custodian Trustee Pty Ltd (name and ACN) | After the date of the contract | $750 |

| Queensland | Custodian Trustee Pty Ltd (name and ACN) ATF Custodian Trust (name of trust) | Before or the same date as the date of the contract | Nil |

| Tasmania | Custodian Trustee Pty Ltd (name and ACN) | After the date of the contract | Nil |

| South Australia | Custodian Trustee Pty Ltd (name and ACN) | After the date of the contract | Nil |

| Western Australia | Custodian Trustee Pty Ltd (name and ACN) ATF Custodian Trust (name of trust) | Before or the same date as the date of the contract | Nil |

| ACT | Custodian Trustee Pty Ltd (name and ACN) | After the date of the contract | Nil |

| Northern Territory | Custodian Trustee Pty Ltd (name and ACN) ATF Custodian Trust (name of trust) as bare trustee for SMSF Trustee Pty Ltd (name and ACN) ATF SMSF (name and ABN of fund) | Before the date of the contract | $5 |

Note: This is a guide only and not legal advice. You should seek legal advice from your property solicitor regarding the name on the contract of sale.

Is a Bare Trust Liable for Land Tax?

No, the Bare Trust itself is not liable for land tax in New South Wales. Under the Duties Act, when a property is held in a Bare Trust, the law looks through the legal title held by the Bare Trustee and treats the ultimate beneficial owner—usually the SMSF—as the actual owner for duty purposes, including landholder duty. This means it’s the beneficial owner, not the Bare Trustee, who is responsible for any land tax obligations.

The role of the Bare Trustee is limited to holding the legal title to the property, and it has no beneficial interest in the asset. Because of this, any liability for land tax, duty, or reporting falls to the person or entity that truly benefits from the property—the SMSF in most cases.

In most Australian states and territories, trustees are generally required to submit the Bare Trust Deed to the relevant State Revenue Office when acquiring property, to ensure correct land tax assessment and compliance. For example, In New South Wales, when a property is purchased through a Bare Trust, the SMSF, as the beneficial owner, will register for land tax—not the Bare Trustee. Even though the trustee holds legal title, it’s the SMSF that benefits from the property and is therefore responsible for any land tax obligations. Revenue NSW treats a Bare Trust as a fixed trust, meaning the beneficial owner (the SMSF) is seen as the true owner for land tax purposes. It’s always a good idea to check with your legal advisor and have them register for land tax on your behalf.

Note – Please check with your legal advisor or state revenue office, as rules can vary between jurisdictions and may change over time.

Conclusion: Navigating the rules around Bare Trusts and SMSF property purchases can be complex, especially when it comes to compliance with borrowing restrictions, land tax, and legal documentation. Getting the structure right from the beginning is essential to avoid costly mistakes. If you’re considering buying property through your SMSF or need help understanding your obligations, don’t leave it to guesswork. Contact the SMSF and property tax specialists at Investax for expert guidance tailored to your situation. We’re here to help you stay compliant while maximising your investment opportunities.

Book a Tax Strategic Consultation with Investax to understand how the right tax structure, planning, and long-term strategy can help you minimise tax, protect your assets, and make smarter financial decisions before costly mistakes are made. Whether you are investing in property, growing a business, or planning your next financial move, getting advice upfront can make a significant difference.

Book Your Strategic Consultation

General Advice Warning

The material on this page and on this website has been prepared for general information purposes only and not as specific advice to any particular person. Any advice contained on this page and on this website is General Advice and does not take into account any person’s particular investment objectives, financial situation and particular needs.

Before making an investment decision based on this advice you should consider, with or without the assistance of a securities adviser, whether it is appropriate to your particular investment needs, objectives and financial circumstances. In addition, the examples provided on this page and on this website are for illustrative purposes only.Although every effort has been made to verify the accuracy of the information contained on this page and on our website, Investax Group, its officers, representatives, employees and agents disclaim all liability [except for any liability which by law cannot be excluded), for any error, inaccuracy in, or omission from the information contained in this website or any loss or damage suffered by any person directly or indirectly through relying on this information.